Budget 2025: Mar-o-Lago! Stay the course on your retirement fund

TNN | Feb 2, 2025, 04.24 PM IST

As more people realise the importance of building a retirement corpus during working years, here is a look at the tax benefits, liquidity and returns that long-term schemes of EPF, PPF and NPS offer

Employees’ Provident Fund Scheme (EPF including VPF)

What is it? All salaried individuals, except govt employees, can use EPF. You and your employer both contribute 12% each of your monthly salary (basic wages, dearness allowance and retaining allowance) every month. But you can choose to put in even up to 100% of your salary towards Voluntary Provident Fund (VPF).

Investment limits: EPF contribution is mandatory for those with monthly salary up to 15,000. If your salary is higher, then EPF is optional. However, this will also depend on the terms of your employment contract.

Liquidity: Both partial and full withdrawal are allowed. If you have retired or resigned (and been unemployed for at least two months after that), you can withdraw the accumulated amount. Partial withdrawals are also allowed for certain circumstances like medical exigency, marriage, etc.

Returns: These are risk-free. For FY 2023-24, the interest rate declared is 8.25%. Interest rate is awaited for FY 2024-25.

Tax benefits: EPF contribution comes within the overall tax deduction limit of 1.5 lakh under Section 80C (not available in new tax regime). As an employee, you are not taxed for the employer’s contribution up to 12% of salary.

Taxability: If your employer’s contribution crosses 7.5 lakh in a financial year, such excess contribution and the income accruing on it is taxable. The same applies if your contribution exceeds 2.5 lakh per annum. Withdrawals before completing five years of continuous service are taxable (subject to exceptions).

National Pension System (NPS)

What is it? If you are non-salaried, you can opt for NPS, which is a voluntary retirement savings scheme for both salaried and non-salaried individuals. Participation is mandatory for govt employees.

Choice of investments: You need to invest at least 1,000 annually in a Tier-I account. Contributions to Tier-II account on an annual basis are not mandatory but any contributions made need to be made in multiples of 250. There is no upper limit but tax benefits are available only till a certain point. Tier-I has limited premature withdrawal options to encourage long-term investing. Tier-II accounts are voluntary and allow withdrawals.

You have a choice of funds to invest in (equity, corporate debt, government securities, alternative investment, etc.) and can switch funds as well as pension fund managers. As per recent guidelines, you can choose up to three pension fund managers for different asset classes.

Liquidity: For a Tier-I account, the lock-in is till superannuation or 60 years of age. You can make partial withdrawals for specified reasons after three years and up to 25% of contributions made. A total of three withdrawals during the entire tenure are permitted. No lock-in for Tier-II account.

Returns: As NPS funds are market-linked, returns are not guaranteed. For example, if you had chosen a Tier-I account in LIC Pension Fund Ltd, your returns would be 12.12% over seven years under Scheme E but 8.80% for Scheme C (as on 31 January 2025).

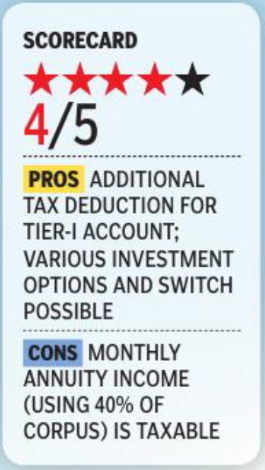

Tax benefits: Tier-I account investments get tax benefits within the overall 1.5 lakh limit under Section 80C. The same benefit for Tier-II account is only for govt employees. However, all subscribers can avail additional tax deduction for investment up to 50,000 in Tier-I account under Section 80CCD (1B) under old tax regime. This benefit has been extended to contributions made in the name of minors under NPS Vatsalya scheme, in the 2025 Budget proposals. There are tax benefits under Section 80CCD (2) if the employer contributes up to 10% of salary (basic+dearness allowance) under the old tax regime. Further, in case of those opting for the new tax regime, tax benefit is available up to 14% of salary (basic+dearness allowance).

Taxability: If employer’s contributions exceed 7.5 lakh in a financial year, taxes will apply on the excess contribution and on income accruing on the same. On superannuation, up to 60% (lumpsum or systematic withdrawal) from accumulated balance is exempt from tax. Monthly annuity is subject to tax.

Public Provident Fund (PPF)

What is it? PPF is a voluntary long-term savings scheme available to both salaried and non-salaried individuals in India. It encourages long-term savings with tax benefits and the safety of a govt-backed investment.

Investment: You can invest between 500 and 1.5 lakh per annum, in lump sum or instalments.

Liquidity: Partial withdrawals are allowed only after six years, based on a prescribed formula. Full withdrawal is permitted only after the 15-year lock-in period. The account can be extended in blocks of five years after the maturity period.

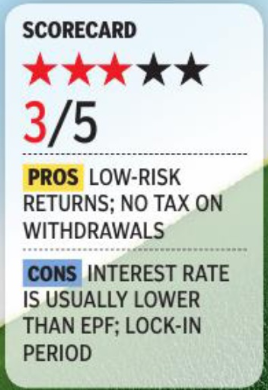

Returns: These are considered low-risk, as PPF is govt-backed. Interest rates are reviewed quarterly, and for rate was 7.1%.

Tax benefits: Within the overall 1.5 lakh under Section 80C under the old tax regime.

Taxability: All withdrawals, and the interest earned, are exempt from tax.

Employees’ Provident Fund Scheme (EPF including VPF)

What is it? All salaried individuals, except govt employees, can use EPF. You and your employer both contribute 12% each of your monthly salary (basic wages, dearness allowance and retaining allowance) every month. But you can choose to put in even up to 100% of your salary towards Voluntary Provident Fund (VPF).

Investment limits: EPF contribution is mandatory for those with monthly salary up to 15,000. If your salary is higher, then EPF is optional. However, this will also depend on the terms of your employment contract.

Liquidity: Both partial and full withdrawal are allowed. If you have retired or resigned (and been unemployed for at least two months after that), you can withdraw the accumulated amount. Partial withdrawals are also allowed for certain circumstances like medical exigency, marriage, etc.

Returns: These are risk-free. For FY 2023-24, the interest rate declared is 8.25%. Interest rate is awaited for FY 2024-25.

Tax benefits: EPF contribution comes within the overall tax deduction limit of 1.5 lakh under Section 80C (not available in new tax regime). As an employee, you are not taxed for the employer’s contribution up to 12% of salary.

Taxability: If your employer’s contribution crosses 7.5 lakh in a financial year, such excess contribution and the income accruing on it is taxable. The same applies if your contribution exceeds 2.5 lakh per annum. Withdrawals before completing five years of continuous service are taxable (subject to exceptions).

National Pension System (NPS)

What is it? If you are non-salaried, you can opt for NPS, which is a voluntary retirement savings scheme for both salaried and non-salaried individuals. Participation is mandatory for govt employees.

Choice of investments: You need to invest at least 1,000 annually in a Tier-I account. Contributions to Tier-II account on an annual basis are not mandatory but any contributions made need to be made in multiples of 250. There is no upper limit but tax benefits are available only till a certain point. Tier-I has limited premature withdrawal options to encourage long-term investing. Tier-II accounts are voluntary and allow withdrawals.

You have a choice of funds to invest in (equity, corporate debt, government securities, alternative investment, etc.) and can switch funds as well as pension fund managers. As per recent guidelines, you can choose up to three pension fund managers for different asset classes.

Liquidity: For a Tier-I account, the lock-in is till superannuation or 60 years of age. You can make partial withdrawals for specified reasons after three years and up to 25% of contributions made. A total of three withdrawals during the entire tenure are permitted. No lock-in for Tier-II account.

Returns: As NPS funds are market-linked, returns are not guaranteed. For example, if you had chosen a Tier-I account in LIC Pension Fund Ltd, your returns would be 12.12% over seven years under Scheme E but 8.80% for Scheme C (as on 31 January 2025).

Tax benefits: Tier-I account investments get tax benefits within the overall 1.5 lakh limit under Section 80C. The same benefit for Tier-II account is only for govt employees. However, all subscribers can avail additional tax deduction for investment up to 50,000 in Tier-I account under Section 80CCD (1B) under old tax regime. This benefit has been extended to contributions made in the name of minors under NPS Vatsalya scheme, in the 2025 Budget proposals. There are tax benefits under Section 80CCD (2) if the employer contributes up to 10% of salary (basic+dearness allowance) under the old tax regime. Further, in case of those opting for the new tax regime, tax benefit is available up to 14% of salary (basic+dearness allowance).

Taxability: If employer’s contributions exceed 7.5 lakh in a financial year, taxes will apply on the excess contribution and on income accruing on the same. On superannuation, up to 60% (lumpsum or systematic withdrawal) from accumulated balance is exempt from tax. Monthly annuity is subject to tax.

Public Provident Fund (PPF)

What is it? PPF is a voluntary long-term savings scheme available to both salaried and non-salaried individuals in India. It encourages long-term savings with tax benefits and the safety of a govt-backed investment.

Investment: You can invest between 500 and 1.5 lakh per annum, in lump sum or instalments.

Liquidity: Partial withdrawals are allowed only after six years, based on a prescribed formula. Full withdrawal is permitted only after the 15-year lock-in period. The account can be extended in blocks of five years after the maturity period.

Returns: These are considered low-risk, as PPF is govt-backed. Interest rates are reviewed quarterly, and for rate was 7.1%.

Tax benefits: Within the overall 1.5 lakh under Section 80C under the old tax regime.

Taxability: All withdrawals, and the interest earned, are exempt from tax.